An Alabama MSP Escapes a 100-Question Renewal

After six years of harder renewals with the same carrier, this $10M MSP switched to UKON and got a shorter application, credit for the compliance work it had already done, a lower premium, and coverage for a risk most policies don't mention at all.

CASE STUDIES

7/8/20264 min read

Six Years of Harder Renewals

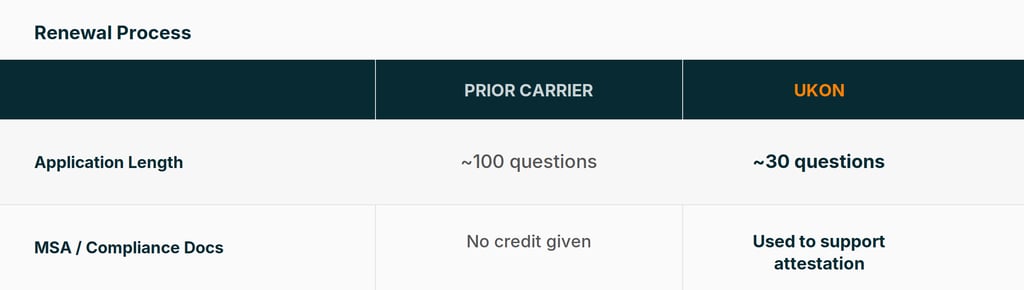

This $10M-revenue MSP had been with the same carrier for six consecutive years. Every renewal, the underwriting got heavier. More questions, more documentation requests, less patience for anything the MSP had already answered the year before. The most recent renewal application ran 100 questions long, and none of it gave any credit for the MSP's existing master services agreement or its compliance and security documentation. Every year, the MSP was effectively starting from zero.

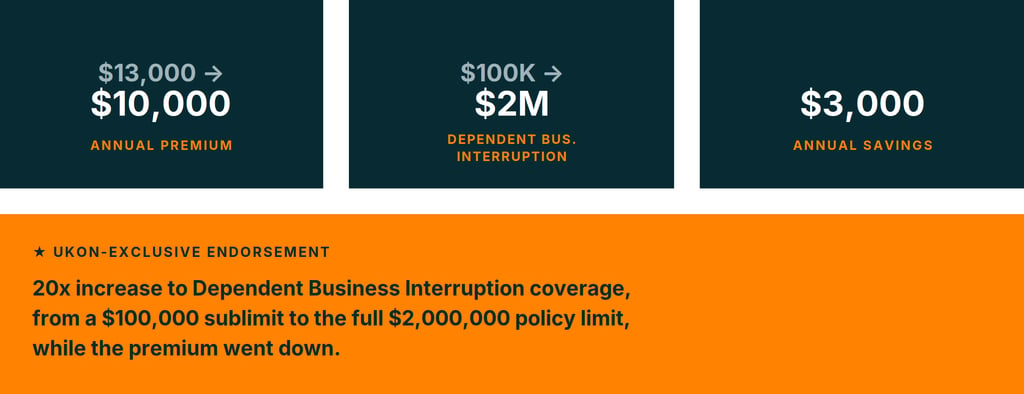

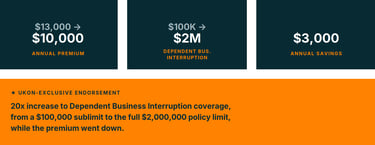

The premium told the same story. The most recent policy carried $2M in coverage for $13,000 a year. Buried inside it, Dependent Business Interruption (DBI), the coverage that protects an MSP's income if a vendor it depends on goes down, was sublimited to just $100,000. A fraction of the MSP's actual exposure if a key vendor went down.

Underwriting That Gives Credit

UKON took a different approach to the same account. The team cut the application down to the questions that actually mattered for this risk. Critically, it used the MSP's existing MSA and compliance documentation to support the attestation, instead of asking the MSP to re-prove what it had already documented.

The Result

UKON took a different approach to the same account. The team cut the application down to the questions that actually mattered for this risk. Critically, it used the MSP's existing MSA and compliance documentation to support the attestation, instead of asking the MSP to re-prove what it had already documented.

The gap this closes:

Without a specific endorsement, a claim arising from an AI agent's autonomous action can land in a gray zone. Arguably a technology error, arguably something the policy never contemplated, and a fight the MSP doesn't want to have with a carrier after a client is already demanding answers.

As MSPs adopt more agentic tooling to scale their own operations, that exposure isn't hypothetical. It grows with every workflow handed to an autonomous system.

An explicit endorsement means the MSP knows, before an incident happens, that this exact scenario is covered.

For an MSP six years into a relationship with a carrier that was asking for more and giving credit for less, the combination of a shorter application, a properly sized DBI limit, a lower premium, and coverage for a risk on the leading edge of how MSPs actually operate today was enough to move the account.

MSPs are increasingly running AI agents inside their own service delivery: automated remediation, AI-driven ticket triage, copilots that can push configuration changes with little or no human review. When one of those agents makes an autonomous decision that causes a client outage, a data loss, or a bad change to production systems, that's a professional liability exposure.

Most tech E&O policies were written before agentic tools existed and simply don't say what happens when the "professional" causing the loss is software the MSP deployed, not a person.

The new policy also added an endorsement for agentic AI-related loss, a coverage that was not available on the prior program and, at the time of placement, was not offered anywhere else in the market.

Why an Agentic AI Endorsement Matters for MSPs

Frequently Asked Questions

What is an agentic AI liability endorsement?

An agentic AI liability endorsement adds coverage for losses caused by an AI agent's autonomous action, such as a bad configuration change, a data loss, or a client outage triggered by an AI tool the MSP deployed. Most standard Tech E&O policies do not include this, because they were written before agentic AI tools existed.

What is Dependent Business Interruption (DBI) coverage?

Dependent Business Interruption (DBI) coverage protects a business against income loss when an outage happens to a third-party vendor it depends on, not just the business itself. For MSPs, this is often one of the most exposed and most underpriced parts of a policy.

Why does Tech E&O underwriting get harder every year for MSPs on the same carrier?

Many carriers add questions and documentation requests at each renewal without giving credit for compliance work or master services agreements the MSP has already completed. This can turn a routine renewal into a 100-question application even when the MSP's risk hasn't changed.

Does standard Tech E&O insurance cover AI agent errors?

Most standard Tech E&O policies do not, because they were underwritten before agentic AI tools were common in MSP service delivery. An explicit agentic AI endorsement is needed to cover losses caused by an AI agent's autonomous decisions.

This case study is intended to show the type of situation that may result in a claim or underwriting outcome and how coverage may respond. It should not be compared to any other account. Whether, or to what extent, a particular loss is covered depends on the facts and circumstances of the loss and the terms, conditions, sublimits, and endorsements of the policy as issued. Availability of the agentic AI endorsement is subject to carrier appetite and underwriting at time of placement and may vary. Prior carrier and program details are shown for illustrative comparison only.

Coverage placed and serviced through UKON's carrier network. UKON is not affiliated with the prior carrier referenced above.

CONTACT

Get in touch with our team.

Follow

Find us

© UKON 2026. All rights reserved.

Pittsburgh, PA

Denver, CO

Bogotá, Colombia