An Alaska MSP Raises Its Coverage Limits and Still Cuts Its Premium

With almost no local specialists writing tech E&O and cyber liability in-state, one Alaska-based MSP had been getting by on a generalist program for years. Moving to UKON closed two of its widest coverage gaps in a single renewal.

CASE STUDIES

7/13/20263 min read

No Specialists On The Map

Alaska's insurance market is thin for any specialty line, and tech errors & omissions and cyber liability are no exception. For this $4M-revenue MSP, that meant working with whatever generalist markets would quote the account, not a broker or carrier that actually understood how an MSP's risk is put together.

The agency had placed the account through the MSP Alliance program, binding coverage with a national carrier through a wholesale broker. It was workable coverage, but built for a typical account in the program rather than shaped around this MSP's actual client base, its dependencies on downstream vendors, or where a single outage could turn into a much larger claim.

Closing The Gap

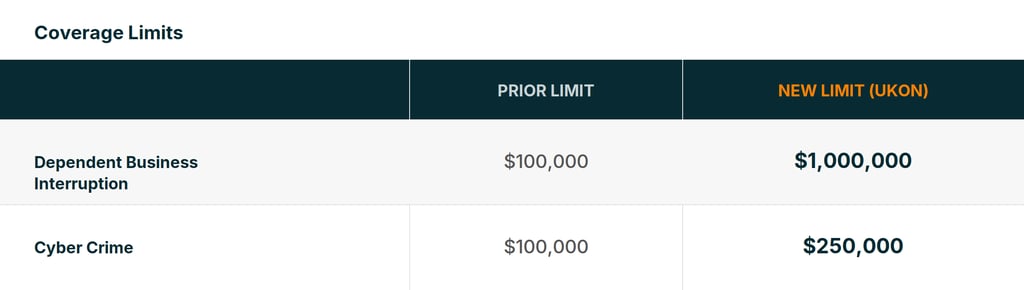

This year, the agency brought the account to UKON. Rather than rewriting the same limits at a lower rate, UKON's cyber specialists reviewed how the MSP's book was actually exposed, starting with two coverages that are frequently underbought relative to real MSP risk: Dependent Business Interruption and Cyber Crime.

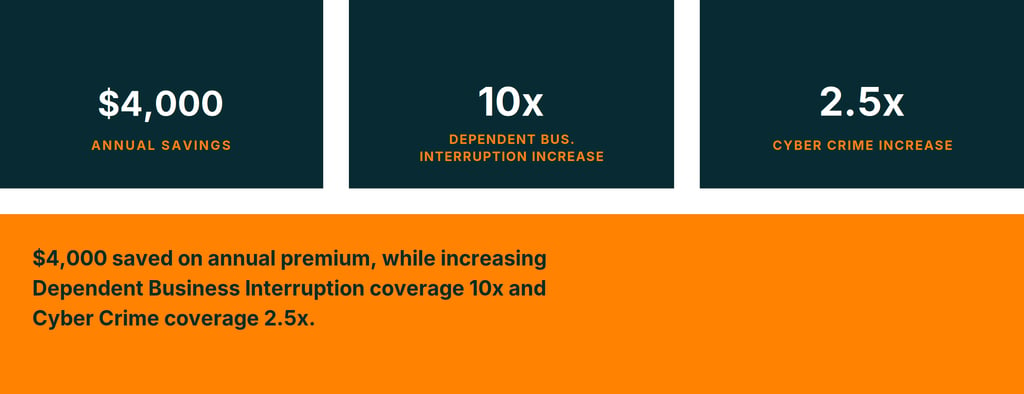

Both limits moved up substantially. A 10x increase in Dependent Business Interruption and a 2.5x increase in Cyber Crime coverage, to better reflect what a real incident, at a vendor the MSP depends on or inside its own funds-transfer process, would actually cost.

The Result

Despite meaningfully higher limits on two of its most important coverages, the MSP's total annual premium dropped.

For an MSP, both exposures scale with the number of clients and systems it touches, which is exactly why default limits so often fall short.

For agencies managing MSP accounts, this case is a reminder to look past the premium line at renewal and ask whether Dependent Business Interruption and Cyber Crime limits actually match the account's real footprint, not just what the prior program happened to quote.

Dependent Business Interruption and Cyber Crime are two of the coverages MSPs most consistently underbuy, often because generalist programs default to round, low limits that were never sized to the account.

A meaningful share of UKON's recent claims activity for MSPs has come from exactly these two coverages: business interruption triggered by an outage at a vendor or downstream provider the MSP relies on, and cyber crime losses from funds-transfer fraud or social engineering.

The agency was able to go back to its client with a stronger renewal story: more relevant coverage, higher limits where it mattered most, and a lower bill, without the account ever having to compromise on protection to hit a price point.

Why This Matters for MSPs

Frequently Asked Questions

What is Dependent Business Interruption (DBI) coverage for MSPs?

Dependent Business Interruption (DBI) coverage protects an MSP against income loss caused by an outage at a third-party vendor or downstream provider it depends on, rather than an outage at the MSP's own systems. It's one of the most commonly underinsured coverages in MSP tech E&O policies.

What is Cyber Crime coverage for MSPs?

Cyber Crime coverage protects an MSP against losses from funds-transfer fraud and social engineering, such as an employee being tricked into wiring funds or redirecting a payment to a fraudulent account. It's distinct from a data breach or ransomware claim.

Why do MSPs often carry low Dependent Business Interruption and Cyber Crime limits?

Generalist insurance programs frequently default to round, low limits that were never sized to the specific MSP's client base or risk footprint. Without a specialist reviewing the account, these limits tend to get renewed year after year without being re-evaluated against actual exposure.

Can raising coverage limits actually lower an MSP's premium?

Yes, when the account is reviewed and repriced based on its actual risk rather than a generic template. This case shows a 10x increase in Dependent Business Interruption and a 2.5x increase in Cyber Crime coverage alongside a lower total premium.

Find out whether your coverage limits match your real exposure.

Request a Risk Management Consult

This case study is intended to show the type of situation that may result in a claim and how coverage may respond. It should not be compared to any other account. Whether, or to what extent, a particular loss is covered depends on the facts and circumstances of the loss and the terms, conditions, and limits of the policy as issued. Prior carrier and program details are shown for illustrative comparison only.

Coverage placed and serviced through UKON's carrier network. UKON is not affiliated with the prior carrier or broker, or the MSP Alliance program, referenced above.

CONTACT

Get in touch with our team.

Follow

Find us

© UKON 2026. All rights reserved.

Pittsburgh, PA

Denver, CO

Bogotá, Colombia