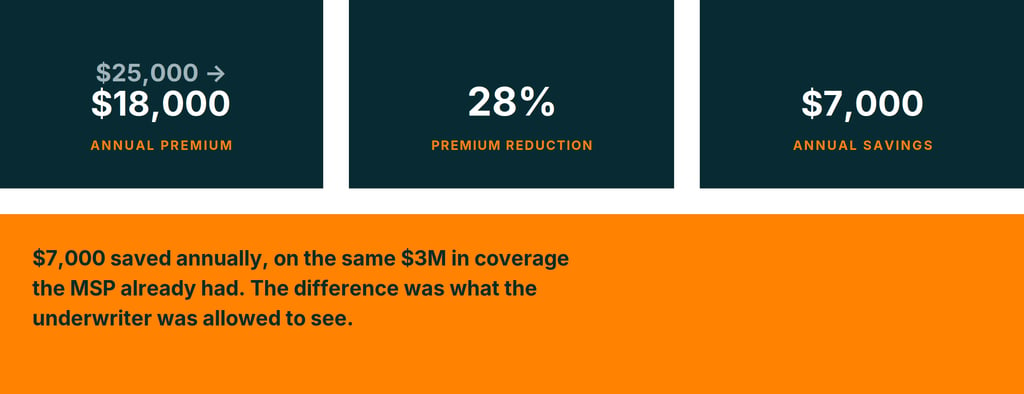

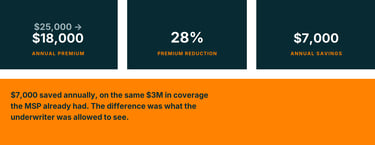

An Arkansas MSP turns its compliance work into a $7,000 premium cut

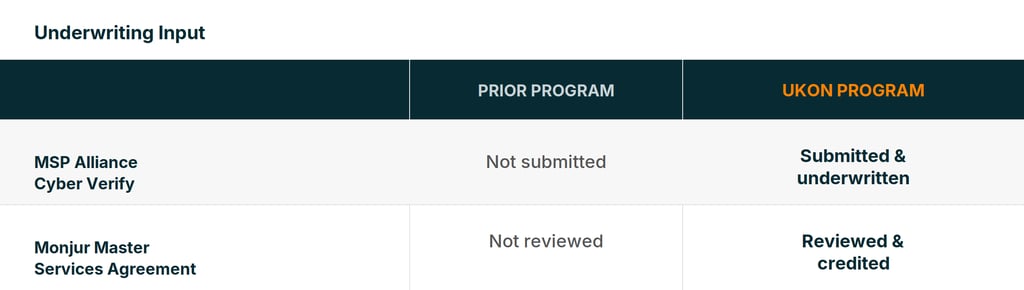

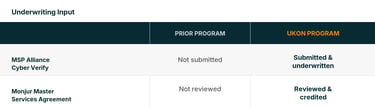

The MSP had already done the work. A completed MSP Alliance Cyber Verify assessment and a properly drafted Monjur master services agreement. Its prior program never asked for either. UKON did, and used them to make the case for a better rate.

CASE STUDIES

7/10/20263 min read

Priced Like Every Other MSP

This $20M-revenue MSP had its tech E&O and cyber liability placed through the MSP Alliance program, bound with a national carrier through a wholesale broker. Coverage was solid on paper: $3M in limits for $25,000 a year.

What the pricing didn't reflect was who the MSP actually was. The company held an MSP Alliance Cyber Verify certification, a third-party assessment of its own security controls, and had standardized its client contracts on a Monjur-drafted master services agreement, which cleanly allocates liability and defines the scope of the MSP's responsibilities. Neither document made it into the underwriting file. The account was quoted as a generic MSP, because that's how it had always been submitted.

Submitting The Whole Picture

When the agency moved the account to UKON, the team asked a different first question: what does this MSP already have that most applicants don't? The answer was Cyber Verify and the Monjur MSA, both submitted alongside the application, not as an afterthought.

UKON's partnership with MSP Alliance and Monjur means these aren't unfamiliar documents to underwrite around; they're part of how UKON evaluates MSP risk.

The Result

Same $3M in limits. A materially lower bill.

With verified security controls and a contractually sound client agreement in hand, UKON took the account to the open market as a stronger-than-average risk, not a standard MSP file, and negotiated from that position.

Underwriters can only price the risk they're shown. Certifications like MSP Alliance Cyber Verify and a well-drafted client MSA like Monjur's aren't just good practice. They're evidence an underwriter can use to justify a better rate, but only if someone puts them in front of the underwriter.

Cyber Verify gives a carrier independent confirmation of the MSP's security posture instead of relying on self-reported answers. A Monjur MSA gives the carrier a clear, defensible allocation of liability between the MSP and its clients. Together, they let an underwriter treat the account as measurably lower risk, which is exactly the leverage UKON used here.

For agencies with MSP clients, the takeaway is simple: before renewal, ask what certifications and contract templates the client already has. If they're not in the submission, the carrier is pricing the account blind, and the client is very likely overpaying.

Why This Matters for MSPs

Frequently Asked Questions

What is MSP Alliance Cyber Verify?

MSPAlliance Cyber Verify is a third-party certification program that independently audits a managed service provider's security controls, governance, and operational maturity. Carriers can use a completed Cyber Verify assessment as independent evidence of an MSP's security posture instead of relying on self-reported answers alone.

What is a Monjur master services agreement?

Monjur is a legal services provider that drafts and maintains master services agreements built specifically for MSPs. A Monjur MSA defines the scope of an MSP's responsibilities and allocates liability between the MSP and its clients, which gives an underwriter a clear, defensible basis for pricing the account.

Why do cyber insurance renewals often ignore an MSP's existing certifications?

Many MSPs are submitted to underwriting the same way every year, using a standard application that doesn't ask about third-party certifications or contract documentation. If a certification like Cyber Verify or a properly drafted MSA isn't specifically included in the submission, the underwriter never sees it and can't price for it.

Can compliance certifications lower an MSP's cyber insurance premium?

Yes, when they're actually submitted and reviewed. Independent certifications and a well-drafted client MSA give a carrier verifiable evidence of lower risk, which an underwriter can use to justify a better rate than a standard, self-reported application would receive.

This case study is intended to show the type of situation that may result in a premium outcome and how underwriting factors may be considered. It should not be compared to any other account. Actual pricing depends on the facts and circumstances of each risk, carrier appetite at time of placement, and the terms and conditions of the policy as issued. Prior carrier and program details are shown for illustrative comparison only.

Coverage placed and serviced through UKON's carrier network. UKON is not affiliated with the prior carrier or broker referenced above, MSP Alliance, or Monjur.

CONTACT

Get in touch with our team.

Follow

Find us

© UKON 2026. All rights reserved.

Pittsburgh, PA

Denver, CO

Bogotá, Colombia